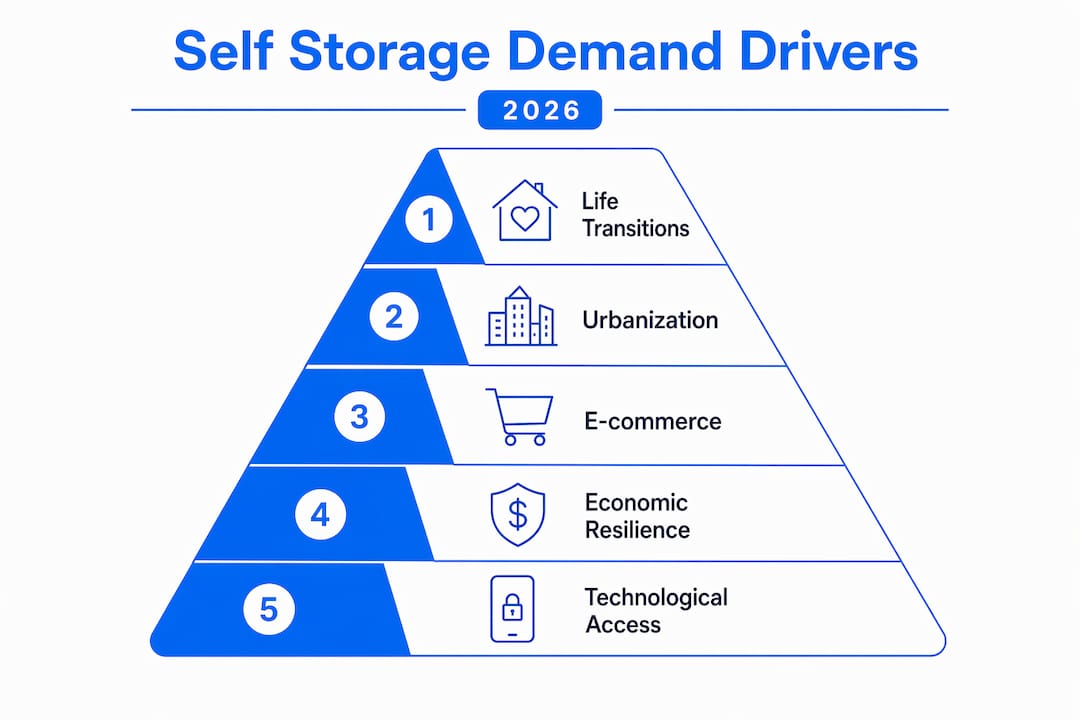

Self-storage demand is the measurable need for additional storage space generated by life transitions, urban living constraints, and business growth, creating consistent occupancy pressure across self-storage facilities nationwide. 33% of Americans currently rent a storage unit, with search interest up 88% since 2020. National street rates average $133 per month as of April 2026, a figure that functions as a real-time economic indicator for the sector. The structural forces behind this demand, most clearly captured in the industry's "6 Ds" framework, make self-storage one of the most defensible real estate asset classes available to investors today.

What is self storage demand, and what drives it?

Self-storage demand is best understood through the 6 Ds framework: Death, Divorce, Downsizing, Dislocation, Deployment, and Disaster. Two additional drivers, Decluttering and Distribution, round out the picture for modern markets. Each of these triggers a predictable, near-immediate need for temporary or long-term storage space, independent of broader economic conditions.

Here is what each driver looks like in practice:

- Death: Estate liquidations require temporary storage while families sort assets, often lasting 6 to 18 months.

- Divorce: Household splits double the storage footprint overnight. One unit becomes two households, each with overflow.

- Downsizing: Retirees moving from a 2,500-square-foot home to a 1,200-square-foot condo cannot shed 30 years of possessions in a weekend.

- Dislocation: Job relocations, lease expirations, and natural disasters all create bridge storage needs.

- Deployment: Military families store household goods during active service, often for 12 to 24 months.

- Disaster: Flood, fire, and storm damage displace residents and contents simultaneously, creating sudden regional demand spikes.

- Decluttering: Consumer culture generates more possessions than most homes can absorb. Storage becomes a pressure valve.

- Distribution: Small e-commerce sellers and last-mile logistics operators use storage units as low-cost inventory hubs.

These recession-resistant demand drivers explain why self-storage occupancy held up during the 2008 financial crisis and the 2020 pandemic disruption, while office and retail real estate collapsed. Life transitions do not pause during recessions. They often accelerate.

Pro Tip: When evaluating a specific market, map which of the 6 Ds are most active locally. A military base nearby means Deployment demand is structural. A coastal city with high divorce rates and downsizing retirees stacks multiple drivers simultaneously.

The e-commerce Distribution driver deserves particular attention. Online sellers on platforms like Shopify, Amazon FBA, and Etsy increasingly use self-storage units as overflow inventory space before shipments scale enough to justify a warehouse lease. This use case is growing faster than most operators realize.

How do market trends and data reflect current demand?

The numbers in 2026 tell a nuanced story. Demand is strong at the consumer level but facing headwinds from two directions: a housing market frozen by the mortgage lock-in effect and a recent wave of new supply that is now moderating.

National street rates averaged $133 per month in April 2026, up 1.5% month-over-month but down 2.2% year-over-year. That year-over-year dip reflects the supply overhang built between 2021 and 2023, not a collapse in underlying demand. The distinction matters for investors reading headline numbers.

| Metric | 2023 Baseline | Early 2026 |

|---|---|---|

| Average tenant stay | 9 to 14 months | 18 to 19 months |

| New supply growth rate | High 20% range | 6 to 8% |

| National street rate (avg.) | ~$136/month | $133/month |

| Consumer search interest | Elevated post-2020 | Up 88% since 2020 |

Tenant stays have lengthened from 9 to 14 months in 2017 to 18 to 19 months in early 2026. This shift is directly tied to the housing market. When people cannot sell their homes or afford to move, they stay put and keep paying storage rent. That is good for occupancy but creates a pricing discipline challenge, since operators cannot rely on move-in specials to drive revenue growth when the tenant base is already locked in.

"Experts expect stabilization in self-storage rent growth in 2026 as supply growth slows and housing turnover eventually increases." — Chilton REIT Research, March 2026

New supply growth has fallen from the high-20% range in 2021 to 2023 down to approximately 6 to 8% in 2025 to 2026. This moderation is the single most important structural signal for investors watching the sector. Tighter supply plus stable demand equals the conditions for rent recovery.

Pro Tip: Track move-in versus move-out rent spreads in your target market. When move-in rents are significantly below move-out rents, operators are discounting to fill units. That negative rent roll spread is a leading indicator of revenue pressure, even when occupancy looks healthy.

How does urbanization shape demand for self-storage?

Urban densification is the structural tailwind that most investors underestimate. Urban residents choosing smaller apartments with limited built-in storage create a permanent, recurring need for external space. Rising real estate prices in cities like New York, San Francisco, and Chicago have compressed average apartment sizes while household possessions have not shrunk proportionally.

The urban on-demand storage market is projected to grow from $4.1 billion in 2026 to $10.2 billion by 2034, a compound annual growth rate of 12.1%. That growth rate is nearly double the broader self-storage sector average. It reflects a specific consumer profile: urban renters without cars, without garages, and without basements who need storage within walking distance or accessible via app-based pickup.

| Format | Traditional suburban facility | Urban micro-facility |

|---|---|---|

| Location | Highway-adjacent, large lot | City core, mixed-use building |

| Unit size | 10x10 to 10x30 dominant | 5x5 to 5x10 dominant |

| Access model | Drive-up, staffed hours | App-based, 24/7 automated |

| Target customer | Homeowners, movers | Renters, freelancers, small businesses |

| Price per sq ft | Lower absolute rate | Higher rate, smaller total bill |

Smaller, automated facilities close to urban cores are disrupting the traditional large suburban model. Operators like MakeSpace and Clutter pioneered the valet storage concept, where the facility picks up and delivers items on demand. This format removes the car-dependency barrier entirely and opens the market to a younger, urban demographic that traditional drive-up facilities never captured.

Freelancers, online sellers, and small businesses are a growing segment of urban storage tenants. A graphic designer storing equipment, a personal trainer storing gear between sessions, or a vintage reseller storing inventory all represent business-use demand that is stickier than residential demand and less sensitive to price.

What do demand drivers mean for investors and operators?

Understanding the forces behind self-storage demand only creates value when translated into specific decisions. Here is how the data maps to operational and investment strategy in 2026.

-

Site selection starts with population thresholds. Institutional developers evaluate minimum trade area populations of 50,000 and specific income metrics before committing to climate-controlled units. Generic per-capita square footage guidelines are outdated. The question is whether the specific population within a 3 to 5 mile radius has the income and lifestyle profile to pay a premium.

-

Climate-controlled units command a 25 to 40% price premium over standard drive-up units. In urban markets where the tenant base skews toward renters storing electronics, clothing, and documents, climate control is not a luxury feature. It is the product.

-

Pricing discipline for existing tenants is now the primary revenue lever. With tenant stays averaging 18 to 19 months, operators who rely on move-in discounts to fill units are leaving money on the table. The focus must shift to structured rate increases for long-term tenants, implemented carefully to avoid triggering move-outs.

-

AI and dynamic pricing tools are no longer optional. Self-storage operators adopting AI for dynamic pricing and expense management are gaining measurable margin advantages over operators still using static rate cards. Tools that adjust pricing based on real-time occupancy, competitor rates, and seasonal demand patterns are now accessible to independent operators, not just REITs.

-

Digital visibility is a demand capture mechanism. When a potential tenant searches "storage near me" or asks an AI assistant for storage recommendations, the facility that appears first captures the booking. Operators who have not structured their digital presence for both search engines and AI tools are invisible to a growing share of demand.

Pro Tip: Review your storage access options against your tenant profile. Urban tenants increasingly expect app-based or keypad access without staffed hours. Matching access format to customer expectations reduces friction and improves conversion.

Key takeaways

Self-storage demand is structurally driven by life transitions, urban densification, and e-commerce growth, making it one of the most defensible real estate asset classes when supply is managed carefully.

| Point | Details |

|---|---|

| The 6 Ds create baseline demand | Death, Divorce, Downsizing, Dislocation, Deployment, and Disaster generate consistent, recession-resistant storage needs. |

| Supply moderation signals recovery | New supply growth falling to 6 to 8% in 2026 sets the stage for rent stabilization and occupancy improvement. |

| Urban demand is accelerating | The urban on-demand storage market is growing at 12.1% CAGR, outpacing the broader sector. |

| Tenant retention requires pricing discipline | Average stays of 18 to 19 months shift revenue strategy from move-in discounts to structured rate increases. |

| Digital and AI visibility drives occupancy | Operators structured for AI search recommendations capture demand that invisible facilities lose to competitors. |

What the data is actually telling investors right now

I have spent considerable time analyzing self-storage market signals, and the pattern I keep returning to is this: the headline numbers look soft, but the structural story is intact. Year-over-year rent declines and softness in Sunbelt markets like Phoenix and Austin are real. They are also the predictable aftermath of a construction cycle that overshot demand between 2021 and 2023.

What concerns me more than the rent dip is the number of operators who are misreading longer tenant stays as a sign of health rather than a sign of housing market paralysis. When existing home sales dropped 8.4% month-over-month in January 2026, the largest decline in nearly four years, that was not good news for storage demand. It meant fewer people moving, fewer life transitions triggering new rentals, and more operators competing for a smaller pool of new tenants.

The opportunity I see is in markets where demographic tailwinds are still intact: secondary cities with net in-migration, aging populations generating Downsizing demand, and urban cores where apartment sizes are shrinking faster than storage supply is growing. Investors who focus on those specific conditions rather than national averages will find better risk-adjusted returns.

The less obvious signal worth watching is AI adoption at the facility level. Operators who get their digital presence structured for AI-generated recommendations now are building a moat that will be very hard to close in two to three years. Most independent operators have not started. That gap is an advantage for those who move first.

— Mike

How Corvanesystems helps operators capture self-storage demand

Understanding what drives self-storage demand is only half the equation. The other half is making sure your facility is visible when that demand converts into a search. Corvanesystems is built specifically for self-storage operators who need to compete in both traditional search and the AI tools that now influence booking decisions. From Google Business Profile optimization to AI visibility audits across ChatGPT, Claude, and Perplexity, Corvanesystems structures your facility's digital presence so it surfaces when tenants are actively looking. A professional digital foundation combined with AI-optimized content turns online discovery into signed leases. See how Corvanesystems can close the visibility gap for your facility.

FAQ

What is self storage demand in simple terms?

Self-storage demand is the measurable need for rentable storage space generated by life events, urban living constraints, and business growth. It reflects how many people and businesses actively require storage units at any given time in a specific market.

Why is self storage popular despite economic uncertainty?

Self-storage demand is driven by life transitions like divorce, downsizing, and relocation that occur regardless of economic conditions. These recession-resistant drivers make the sector more stable than most commercial real estate categories during downturns.

What factors affect self storage demand the most?

The primary factors are the 6 Ds (Death, Divorce, Downsizing, Dislocation, Deployment, Disaster), plus urbanization, housing market turnover, and e-commerce growth. Housing market conditions, particularly the mortgage lock-in effect, have had an outsized impact on demand patterns since 2023.

How does urbanization influence self storage demand?

Urban residents living in smaller apartments with limited storage generate persistent demand for external storage solutions. The urban on-demand storage market is projected to reach $10.2 billion by 2034, growing at 12.1% annually.

What does the self storage market look like in 2026?

National street rates average $133 per month, new supply growth has moderated to 6 to 8%, and 64% of tenants now stay longer than 12 months. The sector is positioned for rent stabilization as the construction overhang from 2021 to 2023 clears.