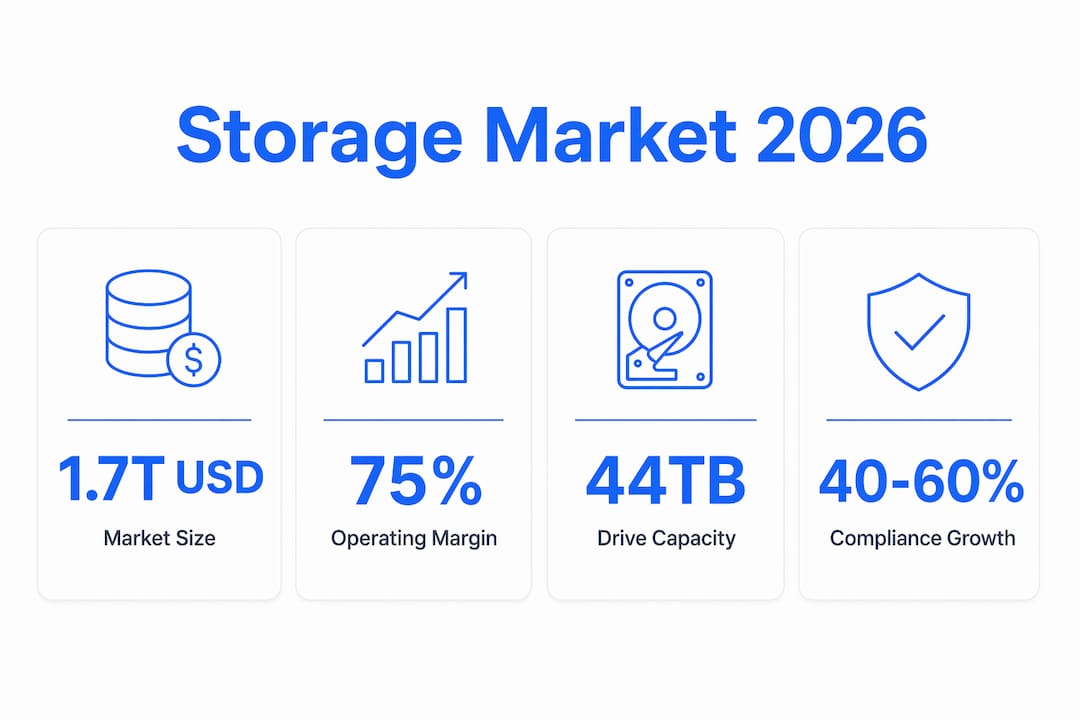

The storage industry keeps growing because AI, regulatory mandates, and structural supply constraints have transformed it from a cyclical commodity market into a core infrastructure sector. This is not a temporary demand spike. The global storage market is projected to reach $1.28 trillion by 2027, a figure that reflects a fundamental reordering of how enterprises, governments, and hyperscalers treat data capacity. For investors and analysts, the key insight is this: storage demand compounds over time in ways that compute demand does not. Every AI model trained, every compliance record retained, and every inference run adds permanently to the total volume that must be stored. Understanding self-storage demand drivers in 2026 requires separating this structural shift from the old cyclical narrative.

Why the storage industry keeps growing: AI and digital transformation

AI workloads create a data loop that never closes. Training a large language model generates massive datasets. Running inference on that model generates more data. Storing multiple versions of training sets, synthetic data, and model checkpoints compounds the volume further. Storage demand is cumulative and persistent, unlike compute demand, which can scale down between jobs. A data center that finishes a training run still holds all the data from that run indefinitely.

The financial evidence is striking. Enterprise SSD revenue for the top five brands reached a record $18.46 billion in Q1 2026, an 86.1% increase quarter over quarter. That jump was driven directly by AI agent services and aggressive procurement by cloud service providers. A single quarter's revenue figure of that magnitude signals that enterprise buyers are not experimenting. They are committing capital at scale.

47% of organizations identify AI data storage management as their primary operational challenge. That statistic matters because it shows the problem is not just volume. It is unpredictability. AI data access patterns are irregular, which makes cost forecasting difficult and pushes organizations toward hybrid and multicloud architectures. Wasabi, AWS, and Azure all report growing enterprise adoption of tiered storage models specifically designed to handle AI workload variability.

- AI training generates multiple dataset versions that must all be retained for reproducibility and auditing.

- Inference runs continuously, producing new data that requires ongoing storage allocation.

- Synthetic data generation for model improvement adds a third, often underestimated, storage layer.

- Hybrid and multicloud strategies spread storage costs but increase management complexity.

Pro Tip: When evaluating storage providers, ask specifically how they price AI workload data. Flat-rate pricing models from providers like Wasabi often outperform egress-heavy models from hyperscalers for AI-heavy use cases.

How compliance mandates expand storage capacity requirements

Regulatory requirements drive storage growth independently of AI. GDPR, CCPA, HIPAA, and SOX each impose specific data retention timelines, and those timelines do not compress as data volumes grow. Financial services firms increased storage capacity by 40–60% over the last five years due to these mandates alone. That figure covers only one sector. Healthcare, legal, and government organizations face comparable or stricter requirements.

The operational impact is direct. A financial institution cannot delete transaction records to free up space. A hospital cannot purge patient records before the legally mandated retention period expires. Storage capacity must grow to accommodate both new data and the accumulating archive of retained records. This creates a floor on storage demand that exists regardless of AI adoption rates.

The industries most exposed to compliance-driven storage growth include:

- Financial services: SOX and SEC rules require multi-year retention of communications, transactions, and audit trails.

- Healthcare: HIPAA mandates patient record retention for a minimum of six years from creation or last use.

- Legal and government: Discovery obligations and public records laws require indefinite retention of certain document classes.

- Technology companies: GDPR and CCPA create both retention and deletion obligations, requiring sophisticated data management infrastructure.

The combination of AI-generated data and compliance-mandated retention creates a compounding effect. Organizations cannot simply archive old AI training data to reduce costs. Regulatory requirements may demand that the data remain accessible and auditable. Storage capacity requirements therefore grow from both ends simultaneously.

Supply-side constraints: who controls storage hardware

Three companies control the majority of global hard disk drive manufacturing: Western Digital, Seagate, and Toshiba. This oligopoly structure limits how quickly supply can respond to demand spikes. High-capacity nearline hard drives are currently in shortage, with supplier lead times running 12–24 months. That gap between order and delivery is the defining supply constraint of the current storage cycle.

The shortage hits different buyers very differently. Hyperscalers like Google, Microsoft, and Amazon have the purchasing power and long-term contracts to secure supply. Small AI labs and academic institutions compete for the same drives but lack the volume commitments that earn priority allocation. This concentration of supply access reinforces the market position of large cloud providers and creates a structural disadvantage for smaller organizations.

| Buyer type | Supply access | Price sensitivity |

|---|---|---|

| Hyperscalers (Google, Microsoft, Amazon) | Priority allocation via long-term contracts | Low: costs passed to customers |

| Large enterprises | Negotiated contracts, moderate lead times | Medium: budget planning required |

| Small AI labs and academic institutions | Spot market, 12–24 month lead times | High: limited purchasing power |

The industry is also shifting from volume-based growth to value-based growth. Higher-capacity drives such as 44TB units improve unit economics without requiring proportional increases in manufacturing output. Western Digital's CFO has stated publicly that the storage boom is still in early stages. That assessment reflects the value-per-unit trajectory, not just shipment volumes.

Pro Tip: Investors tracking storage hardware should monitor nearline HDD lead times as a leading indicator. When lead times compress, it signals either a demand slowdown or a supply expansion. Both have direct implications for pricing power and margins.

Market outlook and financial implications through 2026 and beyond

The financial profile of the storage industry has changed materially. Operating margins are forecast to stabilize at 75–77% between 2026 and 2028, according to JPMorgan's analysis. That range represents historically high levels for the sector. JPMorgan's position is that AI has fundamentally altered how storage companies should be valued, moving them from cyclical commodity producers to strategic infrastructure providers.

The NAND market reflects similar dynamics. Enterprise SSD adoption is accelerating as AI workloads demand faster data access alongside higher capacity. DRAM revenue alone is projected to reach $1.237 trillion by 2028, a figure that illustrates how memory and storage markets are scaling together in response to AI infrastructure buildout.

| Metric | Current or near-term figure | Implication |

|---|---|---|

| Global storage market size | $1.28T–$1.7T by 2027–2028 | Structural, not cyclical, growth |

| Enterprise SSD revenue (Q1 2026) | $18.46B, +86.1% QoQ | AI procurement driving record demand |

| Operating margin forecast (2026–2028) | 75%–77% | Sustained profitability at infrastructure-tier levels |

| Nearline HDD lead times | 12–24 months | Supply constraint limiting access for smaller buyers |

The risks are real and should not be dismissed. Current stock valuations for Western Digital, Seagate, and Micron reflect strong fundamentals, but they also price in continued AI capital expenditure growth. Any slowdown in hyperscaler spending or a breakthrough in AI model efficiency that reduces data generation could compress demand faster than supply adjusts. The reasons people and organizations rent storage are diversifying, which adds resilience, but the premium growth thesis depends heavily on AI infrastructure spending continuing at its current pace.

Key takeaways

The storage industry's growth is structural, not cyclical, driven by AI's cumulative data demands, regulatory retention requirements, and a supply chain that cannot expand fast enough to meet current orders.

| Point | Details |

|---|---|

| AI creates permanent storage demand | Every training run, inference cycle, and synthetic dataset adds to total volume that must be retained indefinitely. |

| Compliance mandates set a demand floor | Financial services firms alone increased capacity 40–60% over five years due to GDPR, HIPAA, SOX, and CCPA. |

| Supply is oligopoly-controlled | Western Digital, Seagate, and Toshiba control HDD manufacturing, with nearline drive lead times at 12–24 months. |

| Margins are at infrastructure-tier levels | JPMorgan forecasts 75–77% operating margins through 2028, reflecting a permanent valuation shift. |

| Value-based growth extends the cycle | Higher-capacity drives like 44TB units improve economics without requiring proportional manufacturing expansion. |

What I keep telling investors who underestimate this sector

Most analysts I speak with still apply the old cyclical framework to storage. They watch inventory builds, model a correction, and wait for the downturn. That framework made sense when storage demand was tied to PC shipments and enterprise refresh cycles. It does not apply when the primary demand driver is continuous AI inference generating data that must be retained permanently.

The detail that changes the analysis is this: storage demand does not reset. Compute demand can scale to zero between jobs. Storage demand only moves in one direction. Every AI workload run today adds to the total volume that must be stored tomorrow, next year, and a decade from now. That compounding characteristic is what JPMorgan is pricing into its margin forecasts, and it is what most equity models still fail to capture correctly.

The supply constraint story is equally underappreciated. Small AI labs and academic institutions are already being priced out of the nearline HDD market. That is not a temporary friction. It reflects a structural imbalance between manufacturing capacity and demand that will take years to resolve. Investors who understand this dynamic can identify which players benefit from the constraint and which are exposed to it.

My concern for the medium term is AI efficiency gains. If model architectures improve to the point where training requires significantly less data, or if inference becomes dramatically more compute-efficient, the data generation rate could slow. That would not eliminate storage demand, but it would reduce the growth rate. Monitoring AI research developments alongside storage hardware lead times gives you the earliest possible signal of a demand shift.

— Mike

How Corvanesystems helps storage operators capture this growth

The storage industry's expansion creates real opportunity for facility operators, but only if customers can find you when they search. As AI tools like ChatGPT, Perplexity, and Google AI Overviews increasingly drive booking decisions, most storage operators remain invisible to the platforms that matter most. Corvanesystems is built specifically to close that gap. We combine traditional SEO with Generative Engine Optimization so your facility surfaces when a potential customer asks an AI assistant where to rent a unit. Our flat-rate service includes AI-optimized content, local search positioning, and monthly visibility reporting. If you want your facility to compete in a growing market, start with Corvanesystems.

FAQ

Why does AI cause storage demand to keep growing?

AI creates a cumulative data loop where training, inference, and synthetic data generation all produce volumes that must be retained permanently. Unlike compute demand, storage demand compounds over time and does not reset between workloads.

How much have compliance regulations increased storage requirements?

Financial services firms increased storage capacity by 40–60% over the last five years due to GDPR, CCPA, HIPAA, and SOX mandates. Healthcare and government sectors face comparable requirements with similarly strict retention timelines.

What is the global storage market projected to be worth?

The global storage market is projected to reach between $1.28 trillion and $1.7 trillion by 2027–2028, with DRAM revenue alone forecast at $1.237 trillion by 2028.

Why are nearline hard drives in short supply?

Western Digital, Seagate, and Toshiba control the majority of HDD manufacturing, and AI-driven demand has pushed supplier lead times to 12–24 months for high-capacity nearline drives. Hyperscalers absorb this constraint more easily than smaller buyers.

What operating margins are storage companies expected to achieve?

JPMorgan forecasts operating margins of 75–77% for the storage sector between 2026 and 2028. That range reflects the industry's transition from a cyclical commodity business to a strategic infrastructure category driven by AI capital expenditure.