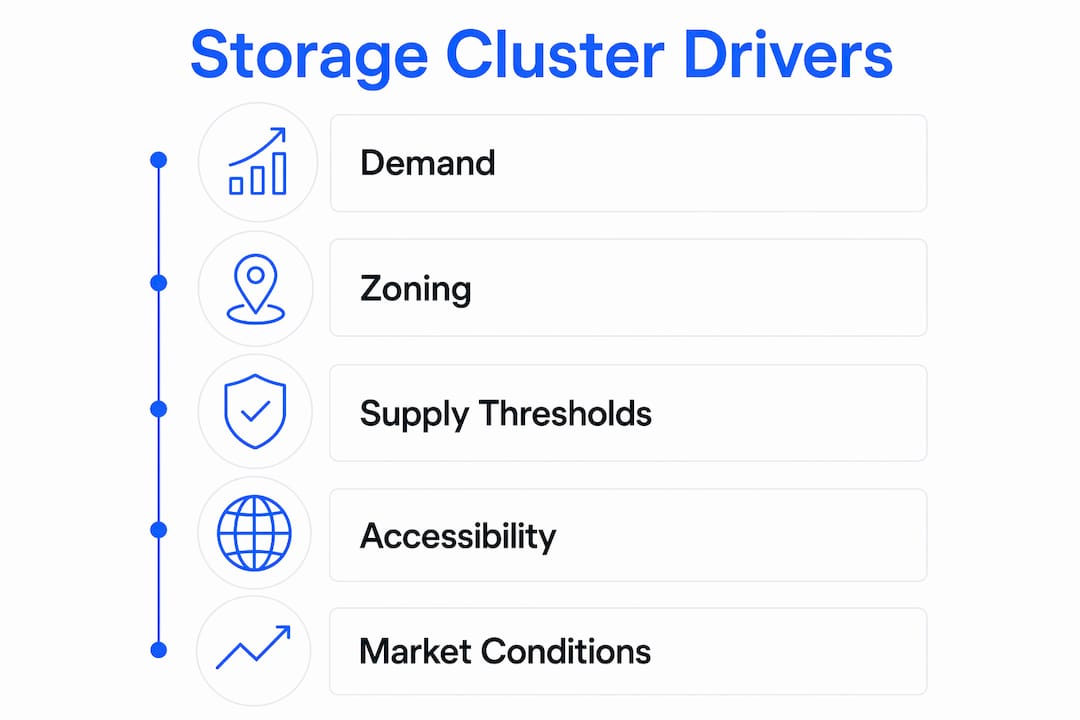

Storage facility clustering is defined as the concentration of multiple self-storage properties within a shared geographic zone, driven by localized demand, zoning constraints, and corridor-based accessibility. This pattern is not accidental. Developers respond to the same market signals, the same permitted land zones, and the same customer behavior, which pulls new builds toward areas where other facilities already operate. For real estate investors, understanding why storage facilities cluster together is the difference between spotting a saturated market and finding an underserved pocket with real upside.

Why storage facilities cluster together: demand and drive time

Storage demand is hyperlocal by nature. Customers choose a facility based on how easy it is to reach, not brand loyalty or price alone. Underwriting frameworks define the primary trade area as a 3–5 mile radius or a 10–15 minute drive time, whichever reflects real-world accessibility more accurately.

That drive-time boundary is where clustering begins. When multiple developers analyze the same dense residential area, they all identify the same primary trade area. Each one builds near the demand center, and the result is a cluster. The facilities are not copying each other. They are independently solving the same location problem.

Physical distance on a map can be misleading. Two nearby facilities can serve entirely different markets if a highway interchange, a river, or a congested arterial road separates them. Operators who model drive-time polygons rather than fixed mile radii get a more accurate picture of which facilities actually compete with each other.

- Customers prioritize access time over raw distance, making drive-time the correct unit of measurement for trade area analysis.

- Natural barriers like rail lines, rivers, and highway on-ramps shrink effective market overlap even between facilities that appear close on a map.

- Dense residential nodes attract multiple developers simultaneously, producing clusters as a byproduct of independent site selection.

- Traffic congestion during peak hours can extend a 2-mile trip to a 20-minute drive, effectively removing a facility from a customer's consideration set.

Pro Tip: When evaluating a site, build drive-time polygons for morning and evening peak hours separately. A facility that looks competitive at noon may be irrelevant to a customer driving home at 6 p.m.

How zoning laws funnel storage into industrial corridors

Zoning is the single most powerful force shaping where storage clusters form. Most municipalities restrict self-storage to industrial or light manufacturing zones. Residential and mixed-use districts rarely permit it. That restriction funnels every developer in a given city toward the same set of available parcels.

Developers follow the path of least resistance through the entitlement process. Industrial corridors already have the permits, the precedent, and the infrastructure. A developer who tries to build storage in a commercially zoned area faces years of variance requests and community opposition. The same developer who targets an established industrial corridor can often break ground within months.

Storage also carries a specific zoning profile that makes it attractive to municipalities with limited commercial land. It generates low traffic, creates few jobs, and requires minimal public services. Zoning experts describe this as a low-amenity commercial use, meaning cities often permit it in zones where higher-traffic retail would be rejected. Storage frequently acts as the first commercial use in a newly permissive zone, establishing a corridor that later attracts additional storage facilities.

Adaptive reuse adds another layer to this dynamic. Converting a vacant big-box retail store or an obsolete warehouse into self-storage lets operators place facilities closer to residential demand without triggering standard zoning restrictions. This approach clusters storage near urban cores and multifamily housing, areas where traditional ground-up development would face rejection.

- Industrial corridors concentrate storage because zoning permits are faster and cheaper to obtain there.

- Adaptive reuse of retail and warehouse buildings bypasses standard zoning hurdles, placing clusters closer to residential demand.

- Frontage and visibility on a major corridor are preferred by operators, limiting viable parcels and pushing facilities toward the same streets.

- Storage's low traffic and job-creation profile makes it a default fill use in zones where other commercial uses are restricted.

What market supply thresholds reveal about cluster size

Operators do not build blindly into a cluster. They use supply-per-capita benchmarks to test whether a market can absorb another facility. The standard threshold is approximately 7 square feet per capita. Markets above that level are considered oversupplied, and new development feasibility drops sharply.

Facility count per population is a second filter. A market with 3 or more facilities per 10,000 residents raises a red flag in most underwriting models. That metric tells an investor how fragmented the existing supply is and how much pricing power any single operator can realistically hold.

Pipeline timing compounds the risk. A cluster that looks balanced today can tip into oversupply within 18 months if two or three permitted projects are under construction simultaneously. Overlapping new developments in the same trade area compress occupancy rates and push street rates down before any of the new facilities reach stabilization.

| Metric | Benchmark | Implication |

|---|---|---|

| Supply per capita | ~7 SF per capita | Above this level signals potential oversupply |

| Facilities per population | 3+ per 10,000 residents | High fragmentation limits pricing power |

| Pipeline window | New builds within 1–3 years | Active pipeline compresses occupancy and rates |

| Drive-time overlap | 10-minute polygon | Defines true competitor set for feasibility |

How corridor frontage and accessibility shape clustering patterns

Prime frontage drives parcel selection, and parcel selection drives clustering. A facility on a high-visibility corridor with easy ingress and egress fills faster than an identical facility tucked behind an industrial park. Operators know this, so they compete for the same limited supply of well-positioned parcels along the same corridors.

Storage's classification as a low-amenity use means it does not need the foot traffic that a restaurant or pharmacy requires. But it does need customers to find it and reach it without friction. That combination, visible but not traffic-dependent, makes arterial roads and highway-adjacent corridors the preferred location type.

The result is a predictable clustering pattern along specific roads. Once one facility establishes itself on a corridor with good access, the next developer targeting the same trade area looks at the same corridor. Available parcels near the first facility become the obvious candidates. The cluster grows parcel by parcel along the same road.

- Identify corridors with permitted zoning, high visibility, and easy access before evaluating individual parcels.

- Map ingress and egress points for each candidate parcel. A facility with a difficult left turn off a busy road loses customers to one with a signalized intersection.

- Check for natural barriers within the corridor. A railroad crossing or a divided highway median can split what looks like one cluster into two separate markets.

- Assess existing facility ages along the corridor. Older facilities with deferred maintenance create an opening for a newer build to capture demand.

- Confirm that frontage visibility is maintained year-round. Tree canopy and seasonal signage obstructions affect customer discovery from the road.

Pro Tip: Use Google Street View to walk the corridor virtually before visiting in person. You will spot ingress problems, visibility gaps, and competing signage that aerial maps miss entirely.

Practical implications for real estate investors evaluating clustered markets

Clustering is not a warning sign by itself. A cluster in an undersupplied market with strong population density is an opportunity. A cluster in a market already at 7 square feet per capita with three projects in the pipeline is a trap. The difference lies in the data you pull before committing capital.

Drive-time market boundaries matter more than street addresses when you assess competition. Two facilities on the same block may compete directly. Two facilities a mile apart, separated by a congested interchange, may serve entirely different customer bases. Reviewing a storage facility location factors checklist before finalizing a site helps investors avoid the most common boundary-definition errors.

Pipeline timing and market saturation require real-time data. Permit databases and certificate-of-occupancy filings are the most reliable sources for tracking what is under construction in a trade area. AI modeling tools now process this data continuously, flagging when a cluster is approaching oversupply before it shows up in street rate data.

- Model drive-time polygons, not mile radii, when defining your competitor set for underwriting.

- Pull permit and pipeline data for all facilities within the primary trade area before finalizing feasibility.

- Evaluate adaptive reuse opportunities in clustered zones. Converting an existing building often costs less and closes faster than ground-up construction.

- Monitor street rates and occupancy quarterly in clustered markets. Rate compression is the first visible signal of oversupply.

- Factor storage pricing strategy into your underwriting model. Clustered markets compress rates faster, so your pro forma needs to reflect realistic street rates, not asking rates.

Key takeaways

Storage facilities cluster together because demand is hyperlocal, zoning restricts development to specific corridors, and operators independently target the same high-visibility parcels within the same drive-time boundaries.

| Point | Details |

|---|---|

| Drive-time defines competition | Use 10-minute drive polygons, not mile radii, to identify true competitors in a cluster. |

| Zoning creates corridor concentration | Industrial zoning funnels multiple developers toward the same permitted parcels, producing clusters. |

| Supply benchmarks signal risk | Markets above 7 SF per capita or 3+ facilities per 10,000 residents face oversupply pressure. |

| Pipeline timing is a hidden risk | New builds within 1–3 years of your target opening compress occupancy before stabilization. |

| Adaptive reuse expands cluster options | Converting retail or warehouse buildings places storage closer to demand without standard zoning barriers. |

What clustering actually tells you about a market

I have reviewed enough storage feasibility studies to know that most investors treat clustering as a negative signal. They see three facilities on the same corridor and assume the market is full. That instinct is wrong more often than it is right.

Clustering tells you where the demand is. Developers do not build in markets without customers. A cluster on an industrial corridor adjacent to a dense multifamily neighborhood is telling you that thousands of households within a 10-minute drive need storage. The question is not whether demand exists. The question is whether the existing supply is meeting it efficiently.

What I watch for in clustered markets is facility age and condition. A cluster of 20-year-old facilities with outdated security, poor lighting, and no climate control is not a saturated market. It is an underserved one. A modern facility with climate control and digital access can take meaningful market share from aging competitors even in a dense cluster.

The other thing I track closely is pipeline data. A cluster that looks balanced today can deteriorate fast if two permitted projects are 12 months from opening. AI modeling tools now flag this risk in real time, which changes how quickly an investor can respond. The operators who monitor permit databases continuously make better decisions than those who rely on annual feasibility reports.

Clustering is a map of where the market has already validated demand. Your job as an investor is to determine whether that demand is being served well, and whether you can serve it better.

— Mike

Corvanesystems helps investors read clustered markets clearly

Storage markets move fast. A cluster that pencils out today can tip into oversupply within a year if you are working from stale data.

Corvanesystems is built for self-storage operators and investors who need accurate, current market intelligence. The platform combines local search positioning, AI-powered content, and visibility auditing to show exactly how facilities appear across Google, ChatGPT, Perplexity, and Claude. For investors evaluating clustered markets, that means understanding not just who your competitors are, but how visible they are to the customers you want. Visit Corvanesystems to see how AI-driven search visibility translates into occupancy in competitive local markets.

FAQ

Why do storage facilities cluster in industrial areas?

Zoning laws restrict self-storage to industrial and light manufacturing zones in most municipalities. Developers target these corridors because permits are faster and entitlement risk is lower than in residential or mixed-use districts.

What is a primary trade area for self-storage?

A primary trade area is the geographic zone from which a facility draws most of its customers, typically defined as a 3–5 mile radius or a 10–15 minute drive time, whichever reflects actual road access more accurately.

How do investors assess oversupply in a clustered market?

Investors use two benchmarks: supply per capita (approximately 7 square feet per capita signals saturation) and facility count per population (3 or more facilities per 10,000 residents indicates high fragmentation and limited pricing power).

Does clustering mean a market is too competitive to enter?

Not necessarily. Clustering confirms that demand exists in a trade area. The real question is whether existing facilities are meeting that demand well. Aging inventory with outdated amenities creates openings for newer builds even in dense clusters.

What is adaptive reuse in self-storage?

Adaptive reuse is the conversion of an existing building, such as a vacant retail store or warehouse, into a self-storage facility. It allows operators to place storage closer to residential demand while avoiding the zoning restrictions that apply to ground-up construction.